Endorsing a check is a critical step in the check-cashing and deposit process, yet it is often misunderstood. An improper endorsement can delay access to funds—or worse, expose you to fraud. Whether you are depositing a paycheck, signing over a check to someone else, or placing limits on how it can be used, understanding endorsement types is essential for safe money management.

Learning how to endorse a check correctly goes hand in hand with endorsing and filling out a check properly, especially as paper checks continue to be used for payroll, refunds, and official payments.

What Does It Mean to Endorse a Check?

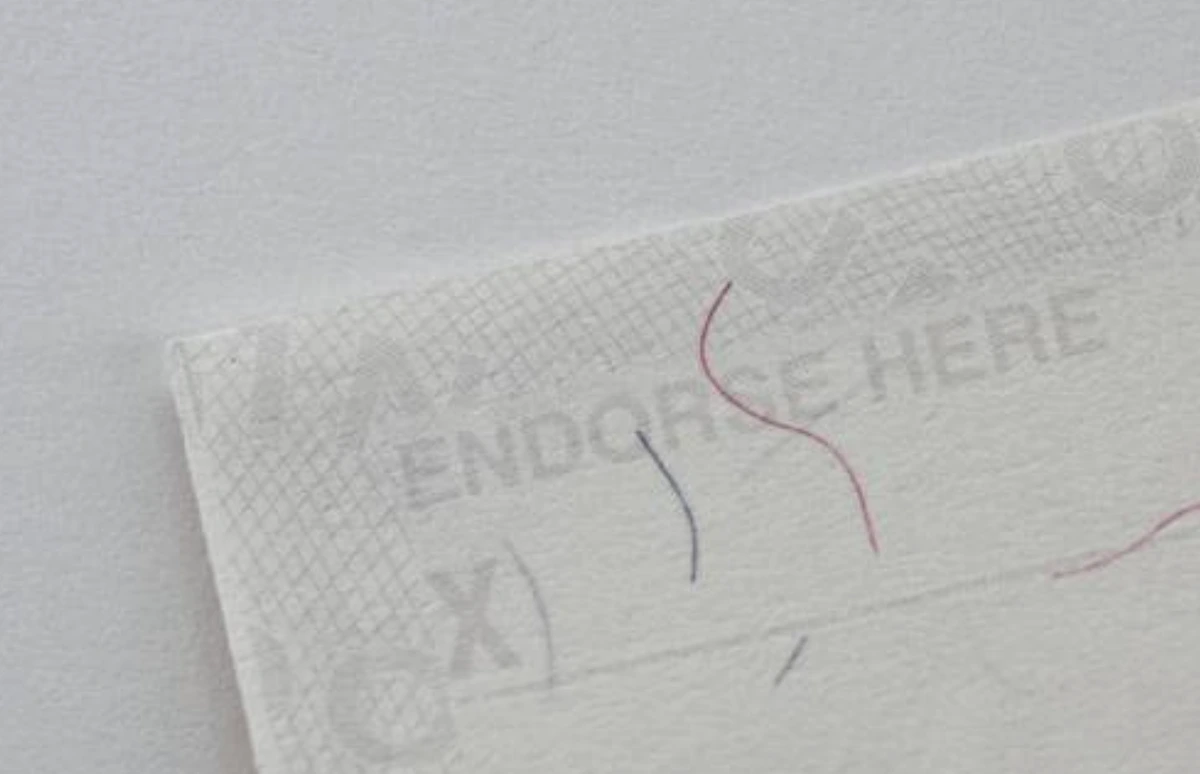

A check endorsement is the signature or instruction written on the back of a check that authorizes how it can be deposited or cashed. By endorsing a check, the recipient confirms they are the rightful payee and specifies how the funds may be transferred.

Banks rely on endorsements to verify ownership, prevent fraud, and ensure the check is processed according to the payee’s intent.

The Three Main Types of Check Endorsements

There are three commonly accepted types of check endorsements, each serving a different purpose.

1. Blank Endorsement

A blank endorsement is the simplest and most commonly used form. It involves signing your name on the back of the check exactly as it appears on the front.

How it works:

- Sign the endorsement line

- Do not add any restrictions or instructions

Pros:

- Easy and fast to use

- Widely accepted by banks

Risks:

- Anyone can cash or deposit the check if it is lost or stolen

Best used when:

You are immediately depositing the check into your own bank account.

2. Restrictive Endorsement

A restrictive endorsement adds instructions that limit how the check can be used. This significantly improves security.

Common examples:

- “For deposit only”

- “For deposit only to account #123456”

Pros:

- Reduces risk of theft or misuse

- Ensures funds go only to a specific account

Cons:

- May take slightly longer to process

- Requires accurate account details

Best used when:

Depositing checks by mail, mobile app, or when security is a priority.

3. Special (or Third-Party) Endorsement

A special endorsement allows you to transfer the check to another person or entity.

How it works:

- Write “Pay to the order of [Name]”

- Sign underneath

Pros:

- Enables check transfer when necessary

Risks:

- Some banks refuse third-party checks

- Higher scrutiny and possible rejection

Best used when:

You need to legally give the check to someone else and have confirmed the bank will accept it.

Common Endorsement Mistakes to Avoid

Even small errors can cause a check to be rejected. Common mistakes include:

- Signing outside the endorsement area

- Using a nickname that does not match the payee name

- Forgetting to include restrictions when required

- Endorsing a check before knowing how it will be deposited

Banks may place holds or refuse processing if endorsement details are unclear or inconsistent.

Why Proper Check Endorsement Still Matters

Despite the rise of digital payments, checks remain widely used for:

- Payroll and reimbursements

- Government and tax refunds

- Insurance settlements

- Business transactions

Understanding endorsement types helps protect your money and ensures smooth processing—especially when combined with knowing how to write, void, and manage checks correctly.

As explained in our complete guide on endorsing and filling out a check properly, each step, from writing the check to endorsing it, plays a role in financial accuracy and security.