What Is Amortization? A Complete Guide to Amortization Schedules, Accounting, Loans, and Real Estate

Amortization is one of the most important concepts in finance, accounting, lending, and real estate. Whether you are managing a business, evaluating investments, purchasing property, or repaying a loan, understanding amortization can help you make more informed financial decisions.

Although the term is commonly associated with loan repayments, amortization also plays a critical role in accounting for intangible assets and financial reporting. This guide explains what amortization is, how amortization schedules work, how amortization is calculated, and why it matters for businesses, investors, and finance professionals.

What Is Amortization?

Amortization is the process of spreading the cost of an asset or loan over a specific period of time.

Depending on the context, amortization can refer to:

- Gradually paying off a loan through scheduled payments.

- Allocating the cost of an intangible asset across its useful life for accounting purposes.

The primary goal of amortization is to match costs with the periods that benefit from them, creating a more accurate picture of financial performance and obligations.

For example:

- A company purchases a patent for $100,000 with a useful life of 10 years. The company may amortize the cost at $10,000 per year.

- A borrower takes out a mortgage and repays it through monthly installments that reduce both interest and principal over time.

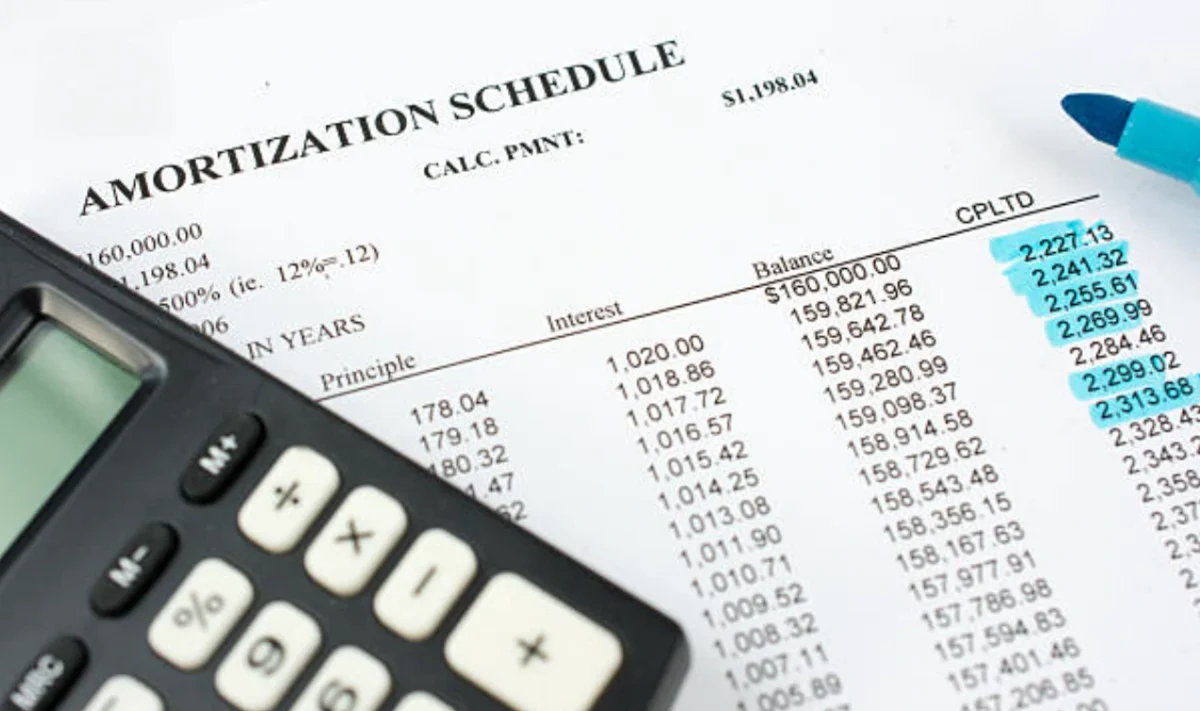

What Is an Amortization Schedule?

An amortization schedule is a detailed table that shows how loan payments are applied throughout the life of a loan.

The schedule typically includes:

- Payment number

- Payment date

- Beginning balance

- Monthly payment amount

- Interest payment

- Principal payment

- Remaining balance

As the loan progresses:

- A larger portion of early payments goes toward interest.

- A larger portion of later payments goes toward principal.

- The outstanding balance gradually decreases until the loan is fully repaid.

Example of an Amortization Schedule

| Payment | Payment Amount | Interest | Principal | Remaining Balance |

|---|---|---|---|---|

| 1 | $1,000 | $600 | $400 | $99,600 |

| 2 | $1,000 | $598 | $402 | $99,198 |

| 3 | $1,000 | $595 | $405 | $98,793 |

This process continues until the balance reaches zero.

What Is Amortization Expense?

Amortization expense is the portion of an intangible asset’s cost recognized as an expense during an accounting period.

Businesses use amortization expense to allocate the cost of assets such as:

- Patents

- Copyrights

- Trademarks with finite lives

- Licenses

- Customer relationships

- Franchise agreements

For example:

If a company acquires a patent for $50,000 with a useful life of 10 years, annual amortization expense equals:

$50,000 ÷ 10 = $5,000

The company records a $5,000 amortization expense each year.

This treatment helps align expenses with the revenue generated from the asset.

What Is Loan Amortization?

Loan amortization refers to the structured repayment of debt through periodic payments over a predetermined period.

Each payment generally consists of:

- Interest expense

- Principal repayment

Common amortized loans include:

- Mortgages

- Auto loans

- Personal loans

- Business loans

In the early stages of repayment, interest consumes a larger share of each payment because the outstanding balance is higher. Over time, principal repayment increases while interest charges decline.

Benefits of loan amortization include:

- Predictable payments

- Clear payoff timeline

- Reduced outstanding debt over time

- Easier budgeting and financial planning

What Is Amortization in Accounting?

In accounting, amortization is the systematic allocation of an intangible asset’s cost over its useful life.

Amortization follows the matching principle, which requires expenses to be recognized in the same period as the benefits they generate.

Examples of intangible assets subject to amortization include:

- Patents

- Copyrights

- Software licenses

- Customer contracts

- Franchise rights

Accounting amortization helps:

- Improve financial reporting accuracy

- Match costs with revenues

- Comply with accounting standards

- Present realistic asset values on balance sheets

Unlike tangible assets, which are depreciated, intangible assets are generally amortized.

What Is Amortization in Real Estate?

In real estate, amortization typically refers to the gradual repayment of a mortgage loan.

A mortgage amortization schedule illustrates:

- Monthly payments

- Interest costs

- Principal reductions

- Remaining mortgage balance

For example, a 30-year mortgage may require 360 monthly payments.

Real estate investors and homeowners use amortization schedules to:

- Track equity growth

- Estimate refinancing opportunities

- Plan property investments

- Understand interest costs

As principal decreases, the owner’s equity in the property increases.

What Is Accumulated Amortization?

Accumulated amortization represents the total amortization expense recognized for an intangible asset since its acquisition.

It functions similarly to accumulated depreciation for physical assets.

Formula

Accumulated Amortization = Total Amortization Expense Recorded to Date

Example

Patent Cost: $100,000

Annual Amortization: $10,000

After 4 years:

Accumulated Amortization = $40,000

Net Book Value = $100,000 − $40,000 = $60,000

Accumulated amortization appears as a contra-asset account and reduces the carrying value of the intangible asset on the balance sheet.

How to Calculate Amortization

The calculation method depends on whether you are amortizing a loan or an intangible asset.

1. Amortization of Intangible Assets

The straight-line method is the most common approach.

Formula

Annual Amortization Expense = Asset Cost ÷ Useful Life

Example

Asset Cost = $60,000

Useful Life = 6 years

Annual Amortization Expense = $60,000 ÷ 6

Annual Expense = $10,000

2. Loan Amortization Calculation

The standard loan amortization formula is:

M = P × [r(1+r)^n] ÷ [(1+r)^n − 1]

Where:

- M = Monthly payment

- P = Loan principal

- r = Monthly interest rate

- n = Total number of payments

This formula determines the fixed payment required to fully repay a loan over a specified term.

Financial calculators and spreadsheet software can perform these calculations automatically.

How to Create an Amortization Schedule in Excel

Microsoft Excel provides a simple way to build a loan amortization schedule.

Step 1: Enter Loan Information

Create input fields for:

- Loan amount

- Interest rate

- Loan term

- Monthly payment

Example:

| Variable | Value |

|---|---|

| Loan Amount | $200,000 |

| Annual Interest Rate | 6% |

| Loan Term | 30 Years |

Step 2: Calculate Monthly Payment

Use Excel’s PMT function:

=PMT(rate/12, years*12, -loan_amount)

Example:

=PMT(6%/12,30*12,-200000)

Excel returns the monthly payment amount.

Step 3: Build Schedule Columns

Create columns for:

- Payment Number

- Beginning Balance

- Payment

- Interest

- Principal

- Ending Balance

Step 4: Calculate Interest

Formula:

=Beginning_Balance*(Annual_Rate/12)

Step 5: Calculate Principal

Formula:

=Payment-Interest

Step 6: Calculate Remaining Balance

Formula:

=Beginning_Balance-Principal

Step 7: Copy Formulas Down

Extend formulas through the entire loan term until the ending balance reaches zero.

The resulting table becomes a complete amortization schedule.

Why Amortization Matters for Business, Investment, and Finance

Understanding amortization provides significant advantages across multiple financial disciplines.

1. Better Financial Planning

Businesses can forecast expenses and cash flows more accurately when amortization costs are properly recognized.

2. Improved Budgeting

Loan amortization schedules help organizations and individuals plan future debt obligations.

3. Accurate Financial Statements

Amortization ensures intangible assets are reflected fairly and consistently in accounting records.

4. Smarter Investment Decisions

Investors evaluate amortization expenses to understand a company’s profitability and asset management practices.

5. Debt Management

Borrowers can assess total interest costs and identify opportunities for refinancing or accelerated repayment.

6. Real Estate Analysis

Property investors use mortgage amortization schedules to estimate equity growth and long-term returns.

7. Regulatory Compliance

Proper amortization helps organizations comply with accounting standards and reporting requirements.

Common Mistakes to Avoid

When working with amortization, avoid these common errors:

- Confusing amortization with depreciation.

- Ignoring accumulated amortization balances.

- Using incorrect useful life estimates.

- Miscalculating interest rates in loan schedules.

- Failing to update schedules after refinancing.

- Recording amortization inconsistently across reporting periods.

Avoiding these mistakes improves financial accuracy and decision-making.

Conclusion

Amortization is a fundamental concept that affects accounting, lending, real estate, investing, and business management. Whether it involves allocating the cost of an intangible asset or repaying a loan through structured installments, amortization helps create financial clarity and predictability.

By understanding amortization schedules, amortization expense, accumulated amortization, and loan repayment calculations, businesses and individuals can make more informed financial decisions. Additionally, tools such as Excel make it easy to calculate amortization and monitor repayment progress.

As organizations increasingly focus on accurate financial reporting and strategic planning, a strong understanding of amortization remains essential for long-term financial success.