Before you can confidently write or deposit a check, it’s important to understand the information printed on it. While checks may look simple, each section serves a specific purpose that helps banks process payments accurately and securely.

This guide breaks down the parts of a check, explaining what each component means, where to find it, and why it matters. Knowing this anatomy reduces mistakes, prevents fraud, and makes check writing much easier.

Why Understanding Check Anatomy Matters

Every check follows a standardized layout used by banks across the United States. When any part is incorrect or misunderstood, it can cause delays, rejected deposits, or even bounced checks.

Understanding the parts of a check helps you:

- Fill out checks accurately

- Verify payments before depositing

- Avoid common banking errors

- Recognize fraudulent or altered checks

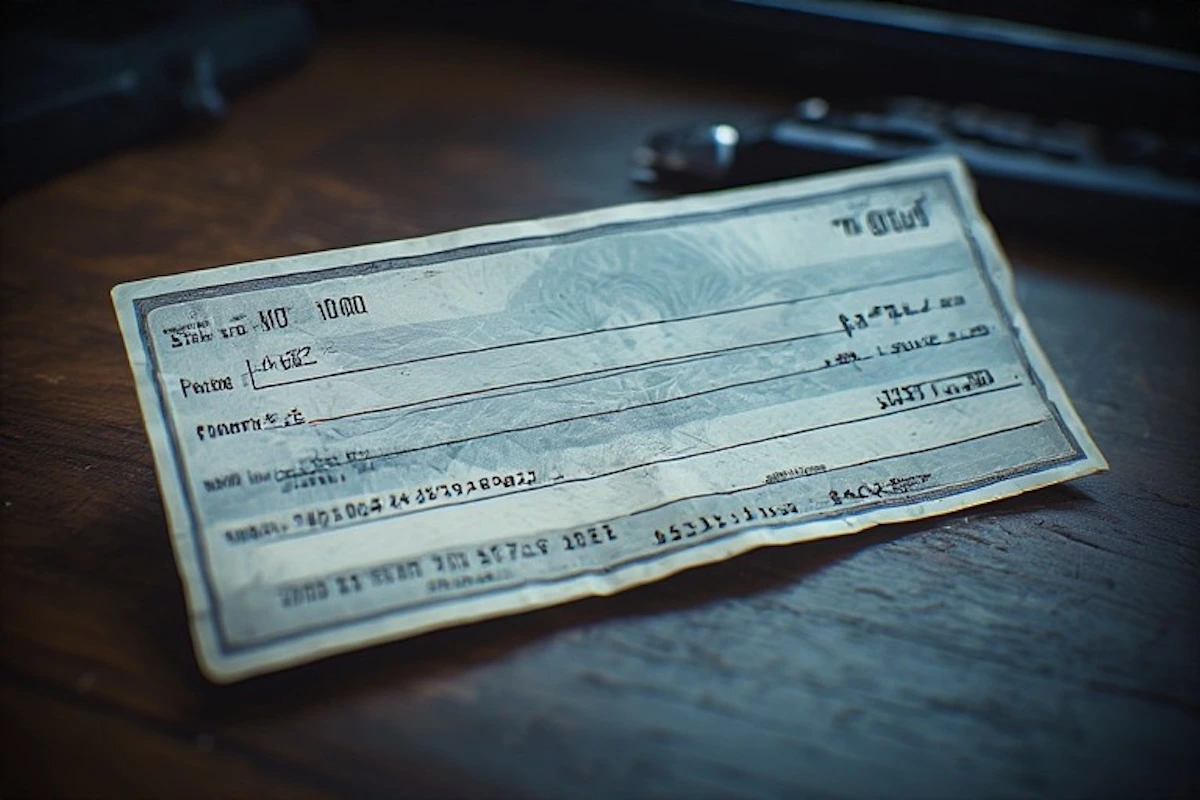

Main Parts of a Check Explained

Date Line

Located at the top right, the date shows when the check is written. Banks use it to determine whether a check is current or postdated.

Payee Line

This line indicates who will receive the money. Only the named payee (or an authorized endorser) can deposit or cash the check.

Numeric Amount Box

This box displays the payment amount in numbers. It allows banks to quickly read the value of the check during processing.

Written Amount Line

The amount is written out in words to confirm the numeric value. If the numbers and words don’t match, banks typically honor the written amount.

Memo Line

The memo line is optional but useful for recordkeeping. It can note the purpose of the payment, such as rent, invoice numbers, or services.

Signature Line

The signature authorizes the bank to release funds from the account. A check without a signature is invalid.

Banking and Identification Numbers on a Check

These numbers are printed at the bottom of the check and are critical to processing.

Routing Number

The routing number identifies the bank or financial institution. It tells the banking system where the funds should come from.

Account Number

This number identifies the specific account the funds will be withdrawn from. It must match the check writer’s bank account exactly.

Check Number

The check number helps account holders track payments and balance their checkbooks. It also helps banks identify duplicate or missing checks.

Where These Numbers Are Used

Banks use the routing and account numbers to:

- Process deposits

- Clear payments

- Detect fraud

- Transfer funds between institutions

This information is why protecting your checks from theft or misuse is so important.

Common Mistakes Involving Check Components

Some frequent errors include:

- Writing incorrect amounts

- Forgetting to sign the check

- Using outdated checks with old account numbers

- Leaving spaces that allow alteration

Understanding each part of a check greatly reduces these risks.

Next Step: Learn How to Use These Parts Correctly

Now that you understand the anatomy of a check, the next step is learning how to properly fill one out from start to finish.

👉 Read the step-by-step guide to writing a check

Related Reading

To further strengthen your understanding of checks and payment methods, explore these helpful guides: