What is a Bill of Sale? Understanding Its Importance and Usage in Business Transactions

In the world of business and personal transactions, a Bill of Sale is an essential legal document that provides proof of the transfer of ownership from one party to another. Whether you’re selling a car, machinery, real estate, or personal goods, a Bill of Sale serves as an official record of the exchange, safeguarding the interests of both the buyer and the seller.

But what exactly is a Bill of Sale, and why is it so important? In this post, we’ll define a Bill of Sale, explain its components, and provide real-life examples to illustrate how it’s used in various business scenarios.

What is a Bill of Sale?

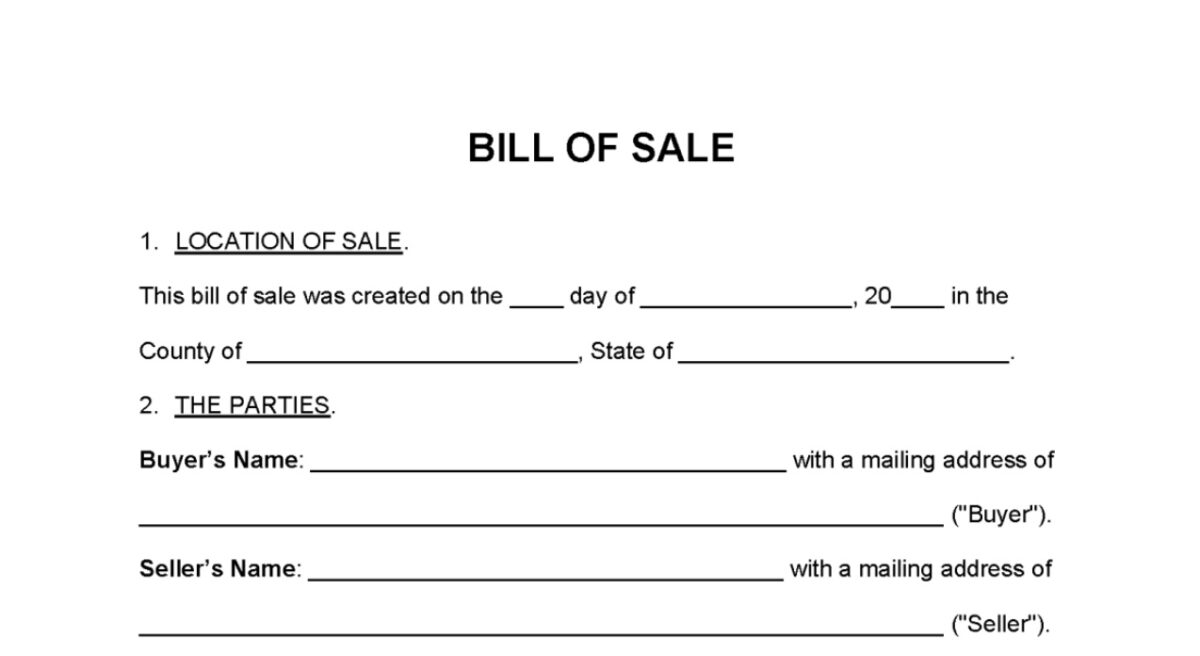

A Bill of Sale is a written document that outlines the details of a transaction involving the sale of goods or property. It serves as evidence that the ownership of an item or property has been transferred from the seller to the buyer. The document typically includes important information about the item being sold, the parties involved, and the terms of the sale.

In essence, a Bill of Sale acts as a receipt for the transaction, ensuring that both parties have a formal record of the exchange. It’s commonly used in a wide range of transactions, from personal sales (like selling a car) to more complex business deals (such as transferring ownership of equipment or inventory).

Key Components of a Bill of Sale

A properly drafted Bill of Sale typically includes the following elements:

- Names and Contact Information of the Buyer and Seller

This section includes the full names, addresses, and contact details of both the buyer and the seller. It establishes the parties involved in the transaction. - Description of the Item or Property

A clear and detailed description of the item being sold is essential. For physical goods, this might include the make, model, year, serial number, or any distinguishing features. In the case of real estate, this section would describe the property, including its address and any relevant legal descriptions. - Sale Price

The agreed-upon sale price is crucial. It must clearly state the amount of money exchanged for the item or property. - Terms and Conditions

This section outlines any specific conditions or warranties associated with the sale. For example, if the item is sold “as-is,” this should be explicitly mentioned. Any guarantees or assurances about the condition or functionality of the item should also be included here. - Date of Transaction

The date on which the sale occurs is important for legal and tax purposes. It marks the official transfer of ownership. - Signatures

Both the buyer and the seller must sign the Bill of Sale. Their signatures indicate that both parties agree to the terms and conditions of the sale. In some cases, the presence of a notary public may be required to verify the authenticity of the signatures. - Witnesses (Optional)

Some Bills of Sale may also include a section for witnesses to sign, although this is not always required.

Types of Bills of Sale

Depending on the nature of the transaction, there are different types of Bills of Sale that are commonly used:

- General Bill of Sale

This is the most common form and is used for the sale of personal property, like vehicles, equipment, or household items. It typically includes all the basic details of the transaction. - Vehicle Bill of Sale

Specifically used for the sale of a car or other motor vehicles. In addition to the standard components, it often includes details about the vehicle’s registration, title, and identification numbers. - Real Estate Bill of Sale

Used for the sale of property or real estate, this version includes detailed descriptions of the property, legal descriptions, and additional legal terms regarding the transfer of ownership. - Bill of Sale for Business Assets

This is used in business transactions where the ownership of tangible assets (like machinery, equipment, or inventory) is transferred. It may also include the transfer of goodwill and intellectual property.

Examples of When a Bill of Sale is Used

1. Selling a Used Car

When you sell a car to another person, a Bill of Sale provides the buyer with proof that they now own the vehicle. It also protects the seller by documenting that the car has been transferred and that the agreed-upon payment has been made.

Example:

- Seller: John Doe, 123 Main St, Springfield

- Buyer: Jane Smith, 456 Oak St, Springfield

- Vehicle Description: 2015 Toyota Camry, VIN: 1234567890

- Sale Price: $8,000

- Date of Sale: March 15, 2024

- Terms and Conditions: “The vehicle is sold as-is, with no warranties or guarantees.”

Both parties sign the document, making it legally binding. The buyer now has proof of ownership, and the seller is protected from any future claims related to the car.

2. Transferring Ownership of Business Equipment

Suppose a business owner is selling a piece of equipment, like a CNC machine, to another company. A Bill of Sale is used to document the transaction and officially transfer the ownership of the equipment.

Example:

- Seller: ABC Manufacturing, 789 Industrial Rd, Springfield

- Buyer: XYZ Corp., 123 Technology Blvd, Springfield

- Item Description: CNC Lathe Machine, Model: ABC-1000, Serial No: 987654321

- Sale Price: $20,000

- Date of Sale: March 25, 2024

- Terms and Conditions: “The equipment is sold as-is. The seller is not responsible for any repairs after the transfer.”

This Bill of Sale serves as proof that the equipment has been sold, protecting both the buyer and the seller in case of any disputes or future claims.

3. Selling Real Estate

In real estate transactions, a Bill of Sale is often used alongside a deed of transfer to document the sale of personal property (like furniture or appliances) that’s included in the real estate deal. It’s not a substitute for a deed but complements the sale process.

Example:

- Seller: Sarah Green, 123 Beach Rd, Palm Beach

- Buyer: Michael Brown, 456 Sunflower Ave, Palm Beach

- Property Description: 123 Beach Rd, Palm Beach, FL 33480, Parcel No: 123-456-789

- Sale Price: $500,000 (real estate) + $20,000 for included furniture

- Date of Sale: April 10, 2024

- Terms and Conditions: “The property is sold with the furniture included in the sale price.”

This Bill of Sale provides a clear record that the personal property (furniture, appliances, etc.) has been included in the transaction and transferred to the buyer.

Why is a Bill of Sale Important in Business?

A Bill of Sale is a fundamental legal document that protects both the buyer and the seller in any transaction. Here are some key reasons why it’s crucial in business dealings:

- Legal Protection: It provides both parties with evidence of the transaction, reducing the risk of future disputes.

- Proof of Ownership: It confirms the transfer of ownership of goods or property, ensuring that the buyer has legal possession.

- Tax and Financial Records: It serves as a record for tax purposes, showing the purchase price and date of the transaction.

- Transparency: It ensures that both parties agree to the terms and conditions of the sale, preventing misunderstandings.

Understand What a Bill of Sale Is About

A Bill of Sale is a simple yet essential document in business and personal transactions. Whether you’re buying a car, selling equipment, or transferring property, a Bill of Sale helps protect both parties by providing a written record of the sale and the agreed-upon terms. By understanding the key components of a Bill of Sale and knowing when to use it, you can ensure smoother and safer transactions in both personal and business settings.

Next time you’re involved in a sale, whether it’s a small business transaction or a larger investment, be sure to draft a Bill of Sale to safeguard your interests and provide proof of ownership transfer.