Compound interest is often called the “eighth wonder of the world” because of its power to grow wealth over time. But when you start saving can make a massive difference in how much you earn. The earlier you begin, the more your money works for you.

In this post, we’ll break down how the age at which you start saving impacts your compound interest earnings, with real-world examples and actionable tips to maximize your returns.

What Is Compound Interest?

Compound interest is the process where your money earns interest, and then that interest earns more interest over time. Unlike simple interest (which only grows on the principal amount), compound interest accelerates your savings exponentially.

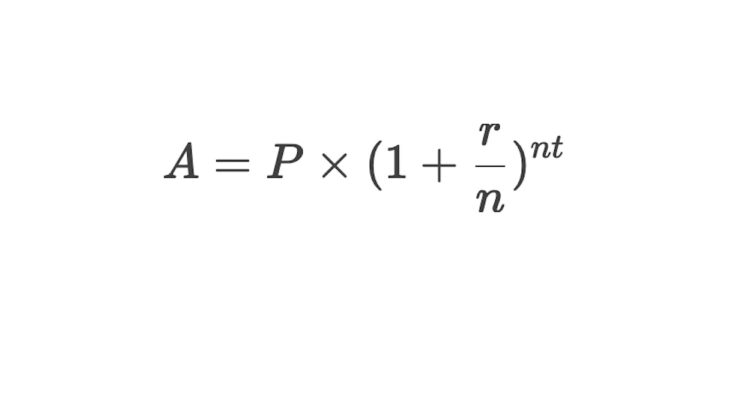

Formula:

- A = Future value

- P = Principal (initial amount)

- r = Annual interest rate

- n = Number of times interest is compounded per year

- t = Time in years

How Starting Age Affects Compound Interest

The key factor in compound interest is time. Even small contributions can grow significantly if given enough years. Let’s compare three savers:

Scenario 1: Starting at Age 25

- Monthly Contribution: $200

- Annual Return: 7%

- Retirement Age: 65

- Total Invested: $96,000

- Final Amount: $525,000

Scenario 2: Starting at Age 35

- Monthly Contribution: $200

- Annual Return: 7%

- Retirement Age: 65

- Total Invested: $72,000

- Final Amount: $245,000

Scenario 3: Starting at Age 45

- Monthly Contribution: $200

- Annual Return: 7%

- Retirement Age: 65

- Total Invested: $48,000

- Final Amount: $104,000

Key Takeaway:

The 10-year delay (25 vs. 35) costs nearly $280,000 in potential earnings. Waiting until 45 reduces gains by over $420,000 compared to starting at 25.

Why Early Savers Win Big

- More Time for Growth – Money invested early has decades to compound.

- Smaller Contributions Go Further – You don’t need to save as much monthly if you start young.

- Less Financial Stress Later – Early savers can retire comfortably without last-minute panic.

How to Maximize Compound Interest

Even if you start late, you can still improve your outcomes:

✔ Increase Monthly Contributions – Save more to compensate for lost time.

✔ Invest in Higher-Yield Accounts – Stocks or index funds typically outperform savings accounts.

✔ Avoid Withdrawals – Let your money grow uninterrupted.

✔ Use Retirement Accounts (401k, IRA) – Tax advantages boost growth.

Final Thoughts

The best time to start saving was yesterday; the next best time is now. Even small, consistent investments in your 20s or 30s can lead to hundreds of thousands more in retirement.

Action Step:

Open a high-yield investment account today and set up automatic contributions—your future self will thank you!